This is a guest blog from SEI: Private Wealth Management, our partner on our latest exhibition From Sea to Shining Sea: 200 Years of American Art.

Supporting the arts tops the list for many philanthropists who want to make an impact on the world. Giving to art and culture offers both a social and educational impact. These same philanthropists are passionate about the arts because they’re passionate about art itself. Similar to experiencing a great work of art, giving, at its core, rewards you emotionally—it simply feels good to give. Coupled with the knowledge that giving contributes to the “greater good,” it seems like a clear win-win.

A downside of the giving effort lies in substantial missed opportunities for alignment between those doing the giving and those organizations doing good service. We believe there is an intersection between art, wealth and the transfer of both with hidden challenges and opportunities to consider.

Valuable Art Collections: An Intersection with Wealth Transfer

Art, antiques and collectibles, particularly for wealthy families, intersect with the wealth transfer world in a few ways. First, these unique assets have value—often significant value—which can increase over time. After all, art value appreciation is a tangible asset that doesn’t correlate with the stock market.1 It is critical, as a collector, to understand what you have, what it’s worth and what you want to do with it. Don’t assume the next generation will want to show off the same Peale or Greek vase just because it’s valuable. Perhaps your antique becomes the method to fund your charitable goals.

Second, if your art is appreciating, so does the exposure to estate tax. Wealthy art collectors have long faced the challenge of passing down art to future generations in a tax-efficient manner. Selling art during their lifetime exposes them to a 20% capital gains tax, while passing works at death triggers inclusion in their estate at full value, exposing them to the 40% estate tax. In recent years, the transfer of art and tax planning became a hot topic when the Houston-based Elkins family (and their tax attorneys) received a significant decision from the U.S. Court of Appeals for the Fifth Circuit.2 The IRS had rejected the Elkins estate settlement, hitting them with a $14.4 million tax bill. But, the Tax Court, backed up by the Appellate Court, validated the Elkins estate plan and supported the family’s contention that the art collection deserved a significant valuation discount, as is allowed for other types of tangible and intangible assets, thereby reducing exposure to millions of dollars in estate tax.

At the root of the tax challenge was a massive art collection, over 64 works by artists including Picasso, Pollock, Cezanne and Twombly, collected for three decades and worth an estimated $24.6 million dollars. This is the first case that extended valuation discounts for minority interests in works of art. In the end, the estate tax refund flowed to the Elkins Foundation, a $210 million endowment that carries on the family’s civic legacy. Obviously, the Elkins family isn’t the typical collector. The case itself is specific and is legally binding on the Fifth Circuit’s jurisdiction only. But, in theory, this ruling could extend to collectors of various wealth levels.

Ultimately, this case shows that there are other estate planning options for your art, antiques and collectibles. Including your art in planning is critical to capture personal goals and tax benefits. The techniques may be complex, but that shouldn’t preclude discussions about how to use art to make an impact on your family and your community—and potentially save some taxes too.

An Unprecedented Amount of Wealth to Pass to Future Generations

Our SEI-sponsored research by the Center on Wealth and Philanthropy at Boston College3 indicates that an unprecedented amount of wealth will pass to future generations over the next 50 years. The good news is that giving is alive and well in America. Unfortunately, the biggest organization to benefit from the transfer of wealth is the U.S. government (even with the recent changes in estate tax law).

Fortunately, wealthy families have an opportunity to reduce estate taxes and control where they’re giving if they take a more proactive approach to planning. And, if they transfer more assets during their lifetime, charities would become the largest benefactors with up to $42 trillion in total wealth transfer—a real opportunity for wealthy families to make a significant impact.

People give for many reasons but tend to give in a big way when there is a personal motivating factor. Philanthropy can be an important unifying force for a family, especially when it aligns with their values and advances their personal or family mission. Doing good together teaches the next generation communication skills, investment policy management, grant-making, entrepreneurial skills and good wealth stewardship. All of these qualities are critical if a family’s wealth and values are to be sustained in future generations.

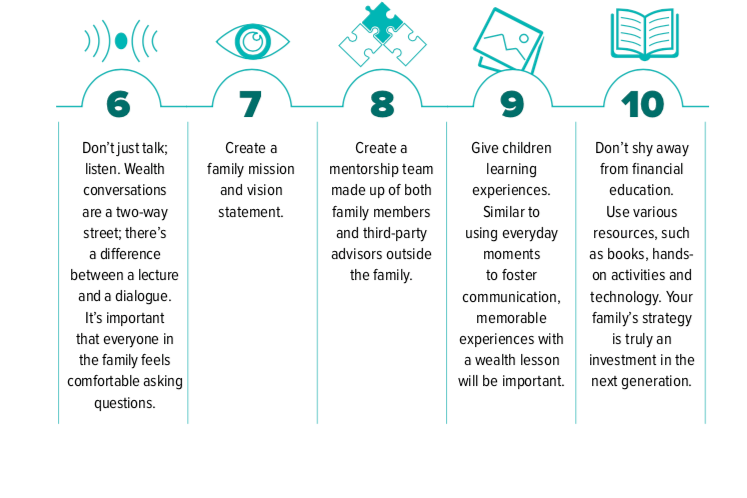

Talk Openly with your Family about your Goals

While complex estate and trust planning can go a long way toward achieving your goals, these plans are often thwarted because of not communicating intentions to family, beneficiaries and future decision-makers. We believe that families who talk openly together about wealth and share in the decision-making process can improve their ability to pass along their financial knowledge and skills to their children or heirs.

A helpful process sometimes referred to as “family governance” can take place in the form of family meetings, ethical wills or casual family conversations. The process should involve financial education, open communication strategies and collaboration. It will be different for every family— but we believe there are best practices everyone should consider to help communicate effectively.

Families who are passionate about art are likely to appreciate true value. They desire to create valuable experiences for their families, they gravitate toward family values about philanthropy and they appreciate the value of their art. The intersection of these topics is best navigated with a few simple suggestions: plan early, recognize the need to continue this perpetual process of planning, and communicate your intentions. If you do this, you can save taxes, achieve your desired impact and preserve your family’s values.